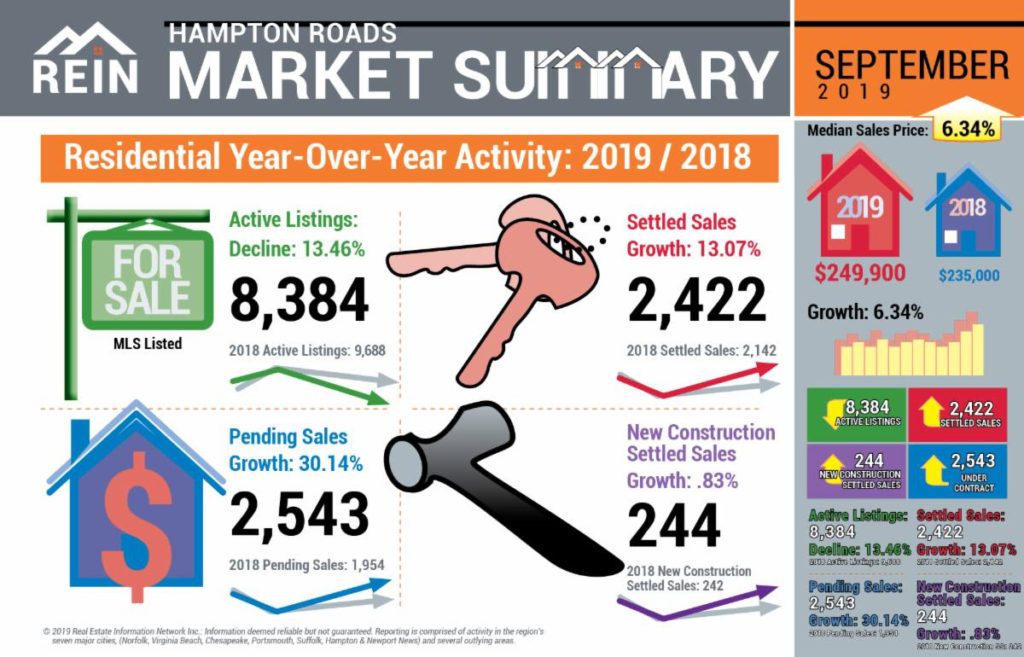

The numbers from Real Estate Information Network (our local MLS) are in for last month and they show some large year over year swings. As you can see on the chart below 30% more homes went under contract in September 2019 than in September 2018.

Check out the increase in the median sale average – it is up 6.34% using year over year numbers (September 2019 verse September 2018). September was also the 50th consecutive month the number of homes for sale has decreased. Showing traffic is still strong and normally doesn’t slow down until Thanksgiving. It will be interesting to see if listings get more showings than normal due to the higher demand from buyers.

We hope that you are enjoying the fall weather! If you want to talk in more detail about how the real estate market impacts your personal situation just reply back to this email or give us call: Lee 757-726-SOLD (7653), Harry 757-434-9084.

Lee and Harry

It’s Not Really Pumpkin After All?

We hate to squash your autumnal dreams, but baking a pumpkin pie might not be as easy as you think. That’s because the canned pumpkin isn’t made of pumpkin at all!

Food & Wine reports that cans of pumpkin puree, even those that advertise “100 percent pumpkin”, are actually made of a range of different squashes. Most pumpkin purees are a mix of winter squashes, including butternut squash, Golden Delicious, and Hubbard. Even the FDA is vague about what counts as “pumpkin,” which allows companies to pack unspecified squashes into their purees and still list pumpkin as the sole ingredient.

Pumpkins might be a quintessential part of autumn but they don’t actually taste that great. Most pumpkins are watery and a bit stringy. Turning them into a puree takes more work and involves less reward, than using other sweeter winter squashes.

While there seems to be a good reason for their deception, we will admit, t’s a little unsettling to find out your favorite pumpkin pie is not what it seems!

If you are a first time home buyer we have good news to share. The VHDA increased their income limits effective September 5th for their first time home buyer loan programs. Qualified first-time homebuyers may receive a percentage of the purchase price to help with the down payment. The maximum grant will be 2 – 2.5 % of the purchase price, based on the down payment required for the eligible VHDA loan. If you are first time buyer, or know someone who is, have them give us a call to discuss this opportunity.

It’s Not Too Early To Think About The Holidays!

Start your holiday shopping at the Seventh Annual Suffolk Artisan Gift Fair!

Visit the Suffolk Visitor Center Pavilion on Saturday, November 23rd from 10am to 3pm and you’ll find festive live music, a petting zoo, face painting and a bounce house. Enjoy light refreshments inside the Visitor Center wander through the Artisan Gift Fair where you will find traditional outdoor holiday market features artisan-quality crafts, jewelry, soaps, fine art, candles, woodcrafts, birdhouses, crocheted items, jams and jellies, totes, holiday ornaments, wreaths, baked goods, seasonal produce, meats and more.

For more information about this event, please contact the Suffolk Visitor Center at 757.514.4130 or www.VisitSuffolkVa.com.

Don’t forget that the Suffolk Farmers’ Market is still open each Saturday now through November 23, 2019.

Shop for fresh locally grown fruits and vegetables, jams and jellies, eggs and milk, meats and poultry, honey, baked goods, pickles and relish, salsa, fresh-cut flowers, and a variety of artisan-crafted goods.

{Re}Stored has come back to Suffolk!Stroll along Main Street on Saturday, November 30th from 10am to 4pm and find handcrafted, homemade and eclectic gifts for those special people in your life. Visit merchants throughout Suffolk’s historic downtown district offering artisan-quality crafts, jewelry, soaps and bath salts, fine art, needlework, ceramics, woodcrafts, crocheted items, jams and jellies, nuts, pottery, totes and handbags, holiday ornaments, home décor, and more. Discounts and holiday specials from other downtown established retailers and restaurateurs’ will be offered as well.

{Re}Stored will be open to the public free of charge. Free parking will be available throughout the downtown area as well.

As part of Suffolk’s “Love Local, Buy Suffolk” initiative, the {Re}Stored event encourages residents and visitors to support owner-operated businesses, as well as support the continued effort of revitalizing the Downtown Suffolk area. Guests to the event will also enjoy complimentary coffee and refreshments, live entertainment, visits from Santa, and so much more!

Selling a house for top dollar is always a team effort between the realtor and the seller and the work starts well before the listing hits the market. Recently, we worked with a seller that wanted to sell but was not quite ready to put the sign in the yard. They took some time, and with our advice, made a few minor changes. That listing is under contract for what will be an all-time high resale price in Kilby Shores if it closes.

As you can see by the statistics below, the market is trending in a direction that is helpful for sellers and, with interest rates staying low, buyers still have a good amount of purchasing power. Last week, one of our listings sold and was the highest priced sale in the neighborhood in over a decade and highest resale price ever in Windsor Woods.

Our local market usually stays decent through Thanksgiving, so if you are thinking about selling you have time to get your home listed and take advantage of the current market. Give us a call, or just reply back to this email and we will come give you a free market analysis on your current home.

Lee 757-726-SOLD (7653) or Harry 757-434-9084

Lee and Harry

It’s Time For The 42nd Annual Peanut Fest

It’s time to celebrate peanuts at the 42nd annual Peanut Fest! Known throughout the Mid-Atlantic for its fun family activities, the festival offers rides, concerts, fireworks, a mud jam, shrimp feast, demolition derby, festival food, peanut butter sculpting, petting zoo, Swamp Roar Motorcycle Rally, pony rides, arts & crafts, corn hole, karaoke, and so much more!

The fun starts on Thursday, October 10, and runs through Sunday, October 13.

General admission:$10 per person. Children 10 & under FREE. Parking is FREE. Debit/credit cards accepted. Early Bird: online only. $7.75 per person + fee.CARLOAD DAY: Thursday, October 10 – one car, van or truck – passengers must be legally seated in vehicle. $40 includes admission + all-you-can-ride wristbands for up to 8 people. MILITARY APPRECIATION DAY: Sunday, October 13 – $5 admission with proper I.D.

Come visit Driver Village for the 26th Annual Fall Festival on October 19th and 20th. You’ll find small-town charm with a blend of historic landmarks and warm southern hospitality. The festival will feature two days of free family fun, including: musical entertainment, a craft beer garden, food, carnival games with pony and train rides, cornhole tournament, Strongwill Kids 1 Mile & 5K Fun Run/Walk and more!

Visit Nike Park on Saturday October 12th for a ghostly good time! There will be family friendly activities and trick or treating from 5pm-7pm, and a Creepy Carnival Haunted Trail from 7pm-9pm.

Suffolk’s Bennett’s Creek Park will transform into a Drive-In Movie Theater and host a showing of Ghostbusters on Saturday, October 19th. Watch two big screens and stay comfy in your car or bring your lawn chairs and blankets and get the best seat in the park. Two full concession areas are available with food and treats with no outside food or drink allowed.

The park is located at 3000 Bennett’s Creek Park Road. Pets are welcome on a leash when outside of your vehicle. The event is always free and open to the public. The movie will begin at approximately 8:15 PM

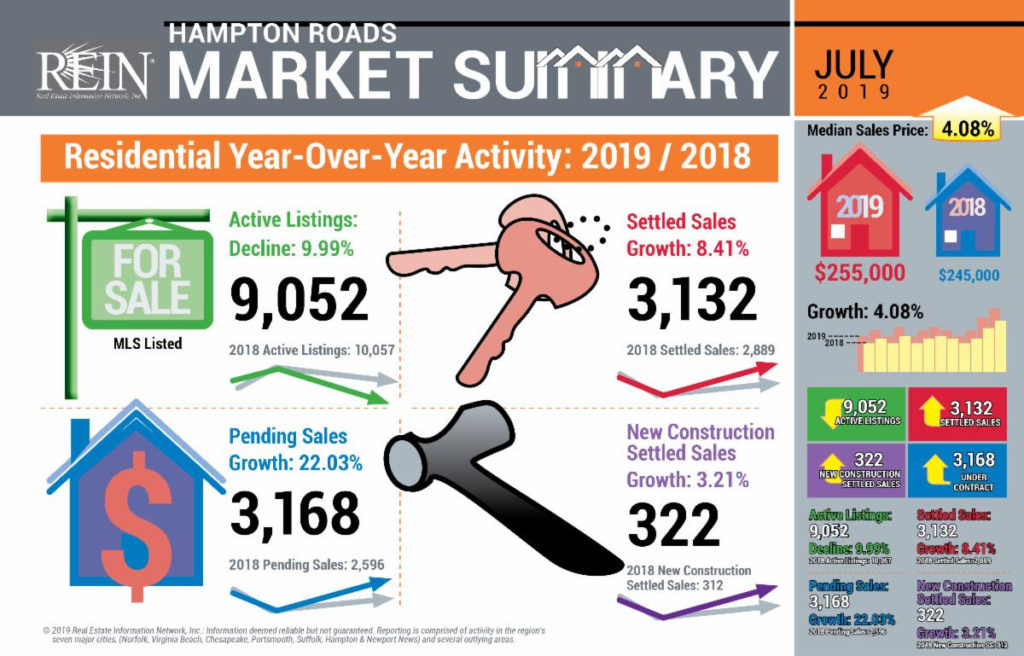

If we were going to make up statistics about our local real estate market that would make a seller happy, they would look something like this:

We didn’t make these numbers up! They are the actual numbers from the Real Estate Information Network (our local MLS). The majority of them are year over year comparables (July 2019 vs.July 2018).

Looking at some other numbers, there is an interesting trend when comparing the numbers for June and July of this year. July had over two thousand fewer active listings than there were in June, but July had a small increase in the number of pending sales (100, roughly 3%) and settled or closed sales (62, roughly 2%).

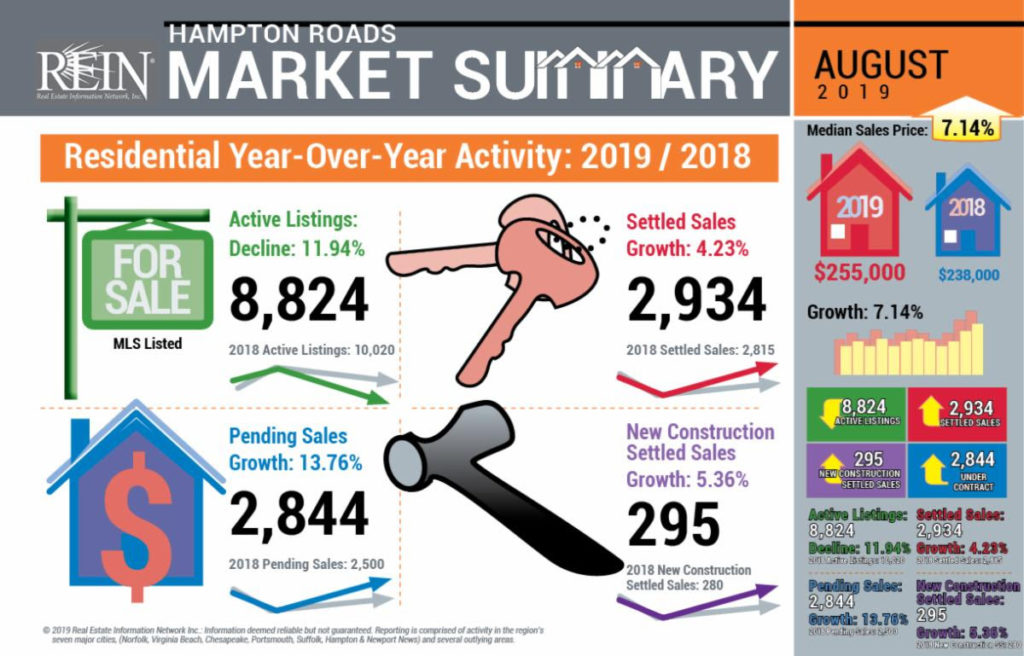

Because the number of listings is down, this is a good time to list your house, especially if it is under $300,000, where inventory is the tightest. It will be interesting to see where the August numbers come in, since it is traditionally one of the slowest months for sales.

We do have some good news for buyers and everyone with a mortgage. If you haven’t checked your current interest rate in the last two or three years, you should read what Bill and Hunter Duggan with Atlantic Bay have to say below.

During the last update we asked: Over the last three years in zip codes 23434, 23437, and 23438 how many houses were listed and sold for more than $600,000? The answer is that 12 homes sold for over $600,000, and Lee was the only agent to have listed and sold more than one of those homes. Whatever your home’s price range is, we are ready, willing and able to help get top dollar for your home.

Give us a call to talk about your options: Lee 757-726-SOLD (7653), Harry 757-434-9084, or just reply back to this email.

Lee and Harry

Grab Your Dog and Go!

Who doesn’t like a walk in the park with your favorite 4 legged friend? So, grab your dog and join your friends and neighbors at Bennett’s Creek Park for the 11th Annual Mutt Strut.

This year’s event will be held at Bennett’s Creek Park on Sunday, September 15, from 11am-4pm promises lots of pet related activities and fun for the entire family, including the four-legged ones. Best of all, it’s free!

Thanks to the generous support of businesses and individuals in our community, Suffolk Humane has been able to make a huge difference for so many animals since it was founded in 2007. Their goal is to raise $35,000 to help make 2019 the best year yet!

Make a plan to spend the day in the park and don’t forget there are lots of pets looking for their fur-ever homes that will be available at the Adopt-a-Thon on Saturday and Sunday, September 14 and 15 at the PetSmart stores in Western Branch and Northern Suffolk.

Interest rates have been moving lower since the start of June and have recently reached the lowest levels we have seen in three years. Not only is it a great time to purchase, it’s a great time to refinance. If you would like to know how much you can afford when purchasing, or how much you can save with refinancing, give me a call.

Bill Duggan, Sr. Mortgage Banker, Atlantic Bay Mortgage Group (757)615-5172 or billduggan@atlanticbay.com

When The Weather Gets Bad

We are heading into peak Hurricane Season and we still have a few weeks left to deal with our usual and sometimes severe thunderstorms. Understanding severe weather terms can help you and your loved stay safe when the weather gets bad.

Hurricane Warning: Hurricane conditions are expected in the warning area within the next 48 hours. Complete your storm preparations. Leave the affected area if directed by local officials–Know your zone.

Hurricane Watch: Issued when a hurricane with sustained winds of 74 mph (65 knots, 118 km/h) or higher is possible.

Severe Thunderstorm Watch: There is a possibility that severe thunderstorms may occur in your area.

Severe Thunderstorm Warning: A severe thunderstorm is occurring or will likely occur soon in your area.

Flash Flood Watch: Due to heavy or excessive rainfall in a short period of time; your area may experience flooding.

Flash Flood Warning: Flash flooding is in progress, imminent, or highly likely. Seek higher ground immediately or evacuate if directed to do so.

Tornado Watch: Tornadoes are possible in your area. Remain alert for approaching storms.

Tornado Warning: A tornado has been sighted or indicated by weather radar. Take shelter immediately.

Prepare For Severe Weather: More steps that you can take to keep yourself and loved ones safe include: An emergency kit prepared with supplies. Include things such as: Alternate fuel source for heating your home, flashlights and batteries, blankets, food that needs no cooking or refrigeration, 3 day supply of water, prescription medicines, battery operated radio, flashlights and cell phone chargers. Prepare your car with emergency supplies. Check batteries in smoke detectors and carbon monoxide monitors. Update important documents: insurance information and home inventory. Store them in your emergency kit or a waterproof container.

Remember, days without power means days without electronic devices. Make sure that you have a written list of important phone numbers and medications!

Who Can Handle Heat and Trivia Question Summer is here, both literally and figuratively in the real estate market. It is sunny and hot outside and our local sales market continues to heat back up as well. Based upon statistics from the Real Estate Information Network (our local MLS), 4,846 homes were listed for sale in May which was an increase of 3.57% from May, 2018. But, even while more homes were listed, May’s supply of inventory was only at 4.03 across Hampton Roads down 8.20% percent from May, 2018. In short, this change is good for sellers. If you list your home today there isn’t as much competition and the average sales price is up 4.27% based on year over year numbers!

While sellers are enjoying the market getting warmer, buyers who are looking for homes listed under $275,000 are in a competitive price bracket. Most buyers in this range are finding that they have to make aggressive offers, forgo asking for a full 3% in closing costs, and still sometimes end up in multiple offer situations. The silver lining for buyers is that interest rates are still good.

We have buyers who are looking for a home, so give us a call, Lee 757-726-SOLD (7653), Harry 757-434-9084, or reply back to this email and we will set up a time to talk.

On another note, we are in the process of hiring a new administrative assistant. There will not be any selling involved and the job is about 75% office work and 25% out and about. The link to the application and job description is listed below. If you know someone that you think might be right for the job please let us know!

This month’s trivia question: Over the last three years in zip codes 23434, 23437, and 23438 how many houses were listed and sold for more than $600,000? These zip codes make up central and southern Suffolk. The winner will get something to help them cool off this summer. You can reply back until July 5 to this email with your answers.

Lee and Harry

Restaurant Week…There’s Still Time to Enjoy

There’s still time to indulge yourself and enjoy Suffolk’s Restaurant Week!

This year’s event promises a savory blend of the city’s signature flavors. Participating eateries offer chef-created delicacies and simple three-course, price fixed menus at the DELUXE ($10 breakfast/$10 lunch/$20 dinner), PREMIER ($15 lunch/$30 dinner) or ULTIMATE ($20 lunch/$40 dinner) levels for lunch and/or dinner.

You don’t need coupons, vouchers or tickets. Just visit participating restaurants and order from the Suffolk Restaurant Week menu at each location. With multiple eateries from which to choose, diners will find an exceptional variety of delicacies.

So get out and enjoy! It’s the perfect time to sample new restaurants or delight in old favorites.

Interest rates are low and combine that with a hot real estate market, you realize it’s a great time to buy! The good news is that according to industry experts, this trend of rates getting lower is expected to continue.

I’m happy to discuss the best mortgage options for you to purchase a new home or to refinance your existing mortgage. Bill Duggan, Sr. Mortgage Banker, Atlantic Bay Mortgage Group (757)615-5172 or billduggan@atlanticbay.com

Music is in the Air with the TGIF Summer Series

The TGIF Summer Concert Series continues at Constant’s Wharf Park & Marina and Bennett’s Creek Park every Friday through the summer.

Enjoy this free and family-friendly event in the park where kids can enjoy the children’s area with bounce houses and there are food and merchant vendors on site. Bring your chair and enjoy a variety of bands.

SCHEDULED BANDS at Constant’s Wharf Park & Marina: June 28 – Schooner or Later July 12 – Party Fins

SCHEDULED BANDS at Bennett’s Creek Park: July 26 – Soul Intent August 2 – Affirmative Groove August 9 – The Deloreans August 16 – Tidewater Drive Band

All Friday concerts are free and open to the public.

Constant’s Wharf Park & Marina is located at 110 W. Constance Road in downtown Suffolk. Bennett’s Creek Park is located at 3000 Bennett’s Creek Park Road in Northern Suffolk.

Over the last couple of updates we have been writing about the months of supply (total number of homes listed for sale divided by the number of homes that go under contract that month) decreasing and the number of homes selling each month increasing. Both of these trends have been going on for years when looking at year over year (March 2019 versus March 2018) statistics from the Real Estate Information Network (our local MLS). Both of these are good for sellers, but of course this isn’t a trend that can continue forever.

The trend almost came to an end last month across Hampton Roads, with the number of homes sold increasing only 1.90% year over year. The months supply is still easily trending downward at 9.73% for the 47th consecutive month of a decrease when using year over year numbers.

Interestingly enough, the trend of increasing sales actually ended on the Southside, and it was only the statistics from Hampton (increase of 31.45%) and Newport News (8.77%) that kept Hampton Roads as a whole in the positive. Also, Suffolk’s months of supply is currently the highest of our local major cities at 4.49 months. This still means the real estate community needs more homes to sell, as an average market is normally thought to be between 5 and 7 months of supply.

Last time we asked a trivia question: 24.08% more homes went pending across Hampton Roads in January 2019 than January 2018, what was the percentage increase for just the homes in Suffolk? The answer is an amazing 50.52%.

Sellers often make the mistake of thinking that summer is the best time to list, but studies show that this isn’t the case. If you are thinking about selling your home, let Cross Realty put our 65 years of local experience to work for you.

Give us a call, Lee 757-726-SOLD (7653), Harry 757-434-9084, or reply back to this email and we will set up a time to talk. We are happy to do a quick, no obligation walk through on your home to tell you what your house could sell for in this market.

Lee and Harry

It’s Back for 2019

Suffolk Farmers Market returns on Saturday, May 4, at the Suffolk Visitor Center Pavilion at 524 North Main Street!

Enjoyed by all, the market features fresh locally grown fruits and vegetables, jams and jellies, eggs and milk, meats and poultry, honey, baked goods, pickles and relish, salsa, fresh-cut flowers, and a variety of artisan-crafted goods. You can also find the Teeny Tiny Farm Petting Zoo, Library2Go, live music by Justin Luke McCurry, a bounce house, and the opportunity to get creative with the Suffolk Art League with special themed days scheduled throughout the season.

Open from 9am to 1pm each Saturday though November 23, 2019 the Market is situated at the corner of Constance Road and North Main Street directly behind the Suffolk Visitor Center. All market activities, admission is free and open to the public.

For questions, please contact the Suffolk Visitor Center at 757.514.4130 or log to VisitSuffolkVa.com for details.

It’s a great time to purchase a home! If you would like to get rates quoted, or to see how much you qualify for, contact me- Bill Duggan, Sr. Mortgage Banker, Atlantic Bay Mortgage Group- 757-615-5172 or billduggan@atlanticbay.com

Suffolk Parks and Recreation….a Top 100!

Did you know that Suffolk Parks and Recreation is now nationally accredited and one of the top best 100 Parks and Recreation agencies in the nation?

From youth sports to senior activities and therapeutic recreation programs, the folks at Parks and Rec can even set you up with a doubles partner for tennis. Don’t forget, Suffolk Parks and Recreation offers 16 walking trails throughout our city. Trails are located in parks, along old railroad tracks and even inside city office buildings. You can find pleasant route to meet your health and recreation goals.

As tax time rolls around, it’s good to know that some of your largest home-related expenses are often tax-deductible – which is great news! Here are the tax breaks you may be able to take advantage of as a homeowner.

1. MORTGAGE INTEREST

This is usually the most significant tax break you’ll receive, since a big chunk of your monthly mortgage payment goes towards paying off interest for a while after your purchase. All of the interest you pay during the tax year will be deductible.

Own a second home? Your interest for that mortgage is also deductible. If you rent out your property part of the year and live in it the other part, you may be eligible to deduct that interest. Just beware, if you live or vacation there less than 14 days out of the year or less than 10% of the number of days you rent it out, the IRS may consider it a residential rental property, eliminating your ability to take an interest deduction.

2. POINTS

When you buy a home, you have the ability to pay “points” to your mortgage lender in order to lower your interest rate. Typically, a point is 1% of the loan price – so if you bought or built a new home that costs $250,000 and you paid your lender for one origination point, you should be able to deduct the $2,500 in closing costs paid, from your taxes the year of the home purchase. Let’s say your lender asks for 1.5%; this would mean you can deduct $3,750 from your taxes the year of the home purchase. Generally, you can also deduct points on the year’s taxes if you took a home equity line of credit in order to make home improvements.

If you refinanced or took out a home equity loan for something other than home improvements, you might have the ability to deduct points as well. However, it usually must be spread over the life of the loan instead of in a single year’s tax return. While it may not provide as big of a tax break, the savings will still add up over time.

3. REAL ESTATE TAXES

You’ll also have another big deduction to take on your tax return – property taxes. No matter where your home is located, you’ll pay some form of real estate tax. If you have an escrow account(most mortgages do), it means you’ve been paying a portion of your total property tax bill for the year as part of your monthly mortgage payment. But don’t fret, you don’t have to keep up with the dollars and cents in order to take this deduction. Your lender will send you an annual statement, which will break down what you’ve paid in taxes and interest and what portion went to your escrow account to be used towards taxes. You can only deduct the amount your lender paid from your escrow towards taxes.

4. ENERGY EFFICIENCY CREDITS

In addition to saving you money on energy costs, making improvements to the efficiency of your home may qualify you for a tax credit. Tax credits are actually somewhat superior to deductions, since they are dollar-for-dollar savings no matter what tax bracket you fall into.

Upgrading your home’s windows, roofing, appliances and more with energy efficient equipment will generally count toward a tax credit of this nature, but it’s important to check with the IRS to be sure, as things can change from year to year.

WHAT’S NOT TAX-DEDUCTIBLE?

You may be wondering if there are any home expenses that are off-limits when it comes to lowering your tax bill – and the answer is yes. Here are just a few things you unfortunately cannot deduct from your tax return:

Insurance premiums, such as comprehensive, fire, or title insurance

Principal paid on your mortgage

Home utilities, such as water, gas, or electricity

HOA dues

Even though not every home expense qualifies you for a deduction, taking advantage of the big-ticket items like interest and property tax deductions can help you save a pretty penny come tax time.

.

For more information about this loan program or to discuss which loan option is best for you, give me a call… Bill Duggan, Atlantic Bay Mortgage Group, 757-615-5172 or billduggan@atlanticbay.com

Do you know what makes an agent successful? We do. Cross Realty welcomes queries from those who are interested in joining our award-winning team. Call Harry today at 757-434-9084 to schedule a confidential meeting.

Specializing in properties in South Hampton Roads, Virginia.